The 18 percent solution and saving Social Security

The 18 percent solution

Scott Bessent, the secretary of the Treasury, in a recent interview almost endorsed my 18 percent solution. He said that the country does not have a revenue problem it has a spending problem – something that many of us have been saying for years. He noted that tax receipts stay around 18 percent while spending had increased from 21 percent to 25 percent of GDP during the Biden years. He wanted to get spending back down to 21 percent. But that insures a deficit of 3 percent forever. So why not spending at 18 percent? I have long suggested that changes in spending not exceed the previous year’s change in GDP unless the president declares a national emergency and the congress approves by two thirds majority.

Why doesn’t Trump just tell his cabinet to propose a budget whose total does not exceed 18 percent of last year’s GDP? He could still sic Musk and DOGE to ferret out fraud and waste within the dollars being spent – although that should be the job for the inspector generals at each agency.

Saving Social Security

Some experts, a lot smarter than me, are saying that the solution to the Social Security “crisis” is a simple one. Just index it to prices rather than wages. One expert says that price indexing will remove 80 percent of the unfunded liability gap over the next 75 years. Here is the reference “How to make Social Security a winning campaign issue” by David C. Rose https://thedailyeconomy.org/article/how-social-security-reform-can-be-a-winning-campaign-issue/

Here is a lightly edited quote from the article

Had price indexing [rather than wage indexing] been implemented, Social Security would have run surpluses every year from 1982 to 2023, except for 2021. There would have been temporary shortfalls starting in 2024, but by 2044, Social Security would have been running surpluses again. Surpluses in Social Security could permit a reduction in the tax rate or allow some of the revenue raised from payroll taxes to support Medicare, which is also running large deficits.

This sounds like a much more reasonable fix than Trump’s idea of exempting Social Security from taxation which would make the problem worse. Lutnick and Bessent are supposed to be smart guys so do it!

One of my ideas is for parents to establish a tax free account for their children at birth. This would be like a 529 plan which is used to help parents pay for college expenses. The monies put in such plans are tax-deferred and the withdrawals are tax free when used for education. Similarly, my idea is to have such a plan for the child’s retirement. The parents would put tax-deferred payments into the plan and when the child joins the workforce, they would continue to put into the plan until they retired. They would never be covered by Social Security. They would never pay into Social Security and never receive a Social Security benefit. The returns from these accounts would be significantly higher than those from Social Security. What if the parents did not establish such an account? They would have to pay into Social Security but would still have IRAs to supplement any Social Security “benefits.”

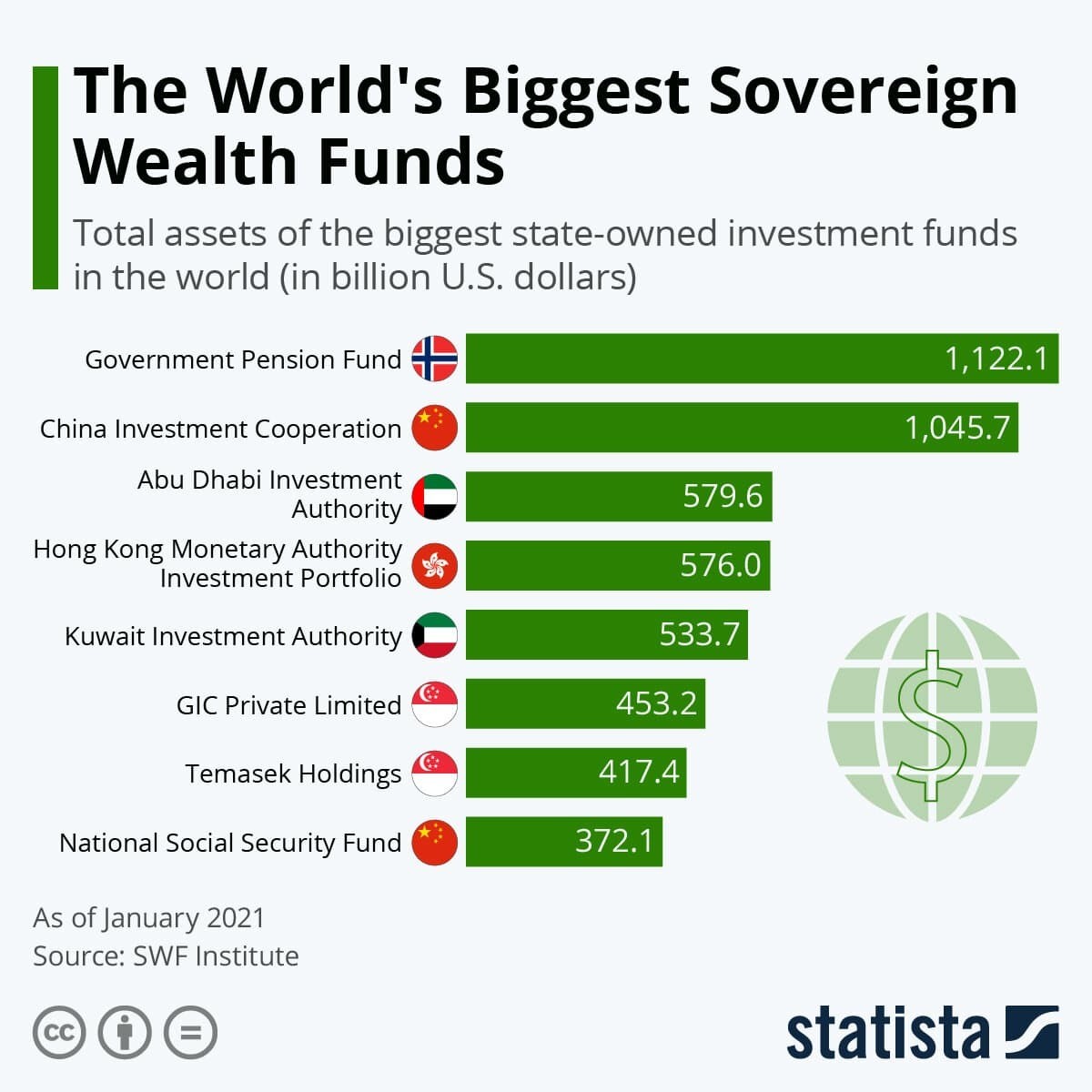

Bessent is also talking about a sovereign fund starting with proceeds from the sale of Fannie Mae and Freddie Mac. The fund would be added to from proceeds from tariffs and other government funds. The monies would be invested and not used until a certain future date and would be designated to fund unfunded liabilities. Australia has such a fund and not surprisingly, demands are being made to use the monies for purposes not originally intended. Such is always the danger when there is a pool of money laying around.

Of course the govt used wage index (1977?) during a time of rising inflation. They would have been eaten alive for the years 1977-1987 (6.7%). I asked AI (Copilot) to check inflation rate vs wage rate from 1977-2017 and both came back around 3.5%. The actual indices may be calculated differently but I figured this might be ballparked?

LikeLike