Federal Reserve Independence and the Constraints of Political Reality

The most recent Federal Open Market Committee (FOMC) meeting provided a instructive case study in the tension between institutional independence and political reality. Despite near-universal consensus among monetary policy models that the federal funds rate warranted an increase, the Committee voted unanimously to hold rates within the existing target range. That outcome was anticipated by futures markets, policy commentators, by me and, evidently, by the Fed itself—yet it stood in direct contradiction to the prescriptions of eleven of the twelve internal models the Fed employs to assess appropriate policy settings.

However, I could have predicted a unanimous vote to hold. Anything else would have Fed watchers and markets screaming that Warsh had lost the committee in his first FOMC meeting and the Fed was in disarray. So despite the divergence between the reserve bank presidents and the Board of Governors preceding the meeting, I expected the committee to be united – this time. However, prior to the meeting, at least four reserve bank presidents made public statements suggesting that a rate increase merited consideration. There is reason to believe that a majority of the twelve presidents, polled privately, would have supported tightening. An exception may be the president of the Federal Reserve Bank of New York, whose proximity to the political and financial centers of power appears to engender a somewhat greater sensitivity to prevailing political pressures. Nevertheless, appearances are important and the Fed has put on a happy face for all to see.

Political Influence on Monetary Policy: Institutional Background

The susceptibility of Federal Reserve governors to political influence is well-documented in the academic literature. Research has consistently demonstrated that governors residing in the Washington, D.C. area exhibit monetary policy preferences more closely aligned with those of the sitting administration and of the Congress—an effect that persists even absent any formal threat to the governors’ tenure or compensation. The structural relationship between the Fed and Congress reinforces this dynamic: the Fed is a creature of Congress, its governors testify before congressional committees and it operates under formal legislative oversight. Presidential commentary on monetary policy, while non-binding, adds an additional layer of pressure. The current administration has been notably outspoken in this regard.

After the meeting of the committee in July 2025 when rates were unchanged the president posted “Jerome ‘Too Late’ Powell has done it again!!! He is TOO LATE, and actually, TOO ANGRY, TOO STUPID, & TOO POLITICAL, to have the job of Fed Chair.” It is in this institutional context that the unanimous vote to hold rates must be interpreted. The decision was not, in all likelihood, a reflection of the committee’s collective assessment of what policy the economic data warranted. Rather, it reflected the practical constraints under which the FOMC operates—constraints that are structural, not incidental.

I would have liked to have been a fly on the wall during the committee’s deliberations. The published minutes will offer only a sanitized summary, but I am confident that a significant portion of the discussion centered on what the models were actually prescribing—and the uncomfortable gap between those prescriptions and the committee’s intended action. Eleven of the twelve Fed models called for a rate increase. When I reviewed those results before the meeting, my immediate reaction was: “They would never dare.” The market reached the same conclusion, and so, evidently, did the Fed itself.

Taylor Rule Prescriptions and Model Evidence

The models underlying the FOMC’s internal deliberations, those of the market and those of academics are largely variants of the Taylor Rule, originally formulated by Stanford economist John Taylor in 1993. The rule provides a systematic basis for setting the federal funds rate as a function of two primary inputs: the deviation of inflation from its target level, and the deviation of real output (or unemployment) from its long-run potential. Formally, the rule prescribes a higher policy rate when inflation exceeds its target or when output runs above potential, and a lower rate under the converse conditions.

Given that inflation has persistently exceeded the Fed’s 2 percent target, virtually all Taylor Rule variants produce recommended rates above the current target range., some significantly so. A simplified heuristic—the “naïve” Taylor Rule—approximates the appropriate rate as current inflation plus two percentage points. At an inflation rate of 4 percent, this implies a federal funds rate of approximately 6 percent.

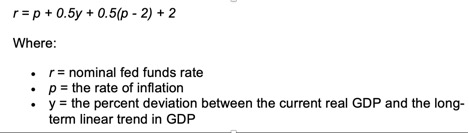

The naïve model that I use in my undergraduate class is:

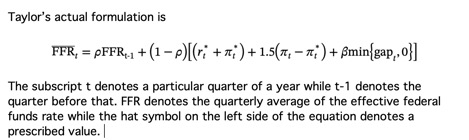

However, Taylor’s original formulation is available from the Atlanta Fed’s data portal and is the one used in my Phd class:

https://www.atlantafed.org/research-and-data/data/taylor-rule

Of all the models surveyed, only one placed the appropriate federal funds rate within the current target range; the rest called for an increase, with one estimate reaching as high as 5.91 percent. Among the variants employed by the Fed, the Holston-Laubach-Williams (HLW) model—published by the Federal Reserve Bank of New York, whose president, John Williams, is a co-author—is perhaps the most widely cited. In its standard form, the HLW model prescribes a federal funds rate of 5.71 percent; the composite of all other variants yields 5.91 percent. When smoothing parameters and price-volatility adjustments are applied, these estimates decline to 3.69 percent (HLW) and 3.79 percent (composite)—with the adjusted HLW estimate falling just within the current target range of 3.50–3.75 percent.

Detailed model outputs are available at:

https://fedagenda.substack.com/p/monetary-rules-report-b79

Implications and Outlook

The policy implications are significant. Should inflation fail to moderate in the coming months, the next FOMC meeting is unlikely to produce a unanimous decision. The structural divide between the Board of Governors—more exposed to political pressure by virtue of their being Washington-based —and the reserve bank presidents, who are institutionally more insulated, is likely to manifest more openly in the vote.

For a comprehensive treatment of the current divergence between model prescriptions and Fed policy, see Matthew Schaffer’s analysis, “Nearly All Monetary Rules Say the Fed Should Raise Rates”:

More broadly, this episode reinforces longstanding concerns about the practical limits of central bank independence. When the Fed’s own quantitative frameworks call for policy tightening and the institution nonetheless holds rates steady, it is difficult to sustain the claim that monetary policy is insulated from political considerations. The most striking historical precedent remains the period in which the Fed maintained near-zero rates as inflation rose first to 4 percent and subsequently to 9 percent—a sequence widely regarded as a consequential policy error. Whether the current committee will demonstrate greater fidelity to its own analytical frameworks remains to be seen.

This is beginning to feel like Trumps Iran strategy. Winning outright is within reach, but then we pull back and let the enemy breathe.

My basic education was that monetary policy focused on getting interests rates above the inflation rate as a dampener until inflation retreated into its 2% long term range. Like most things in this and prior administrations, politicization seeps in and rots the process from the inside-out. The idea of “non-partisan” is a joke, usually told by liberals who want to fool ignorants into believing that bias doesn’t exist in an outcome they prefer.

Warsh MUST stand alone against this ever arrogant know it all president. I wish Jerome Powell had punched him in the face after his comments about “Too late….” Etc. If Warsh wants to make the impact he desires, then he needs to be willing to stand on his bona fides and data, and accept a split board of governors as a sign of productive conflict.

Inflation is the cruelest tax, disproportionately injuring lower incomes with a regressive bodyslam. We owe it to the long term stability of our economy to arrest it. Congress and the supremes must do their parts in ridding this economy of punitive and unwarranted tariffs that suppress free trade and distort markets.

And a side note – Trump’s clown show of a press conference in France this past Wednesday is the most embarrassing moment for a president and a country that I’ve seen in 63 years. The self aggrandizing display of excuses about the Iran MOU was disgusting, and the boot lickers lining up to make excuses for it are equally disturbing.

But did you see Marco Rubio? Clearly displeased. My hope is that he uses the midterms as a good time to honorably resign and create distance before a possible election run. It will take at least a year to diminish the stench but being so close to Trump.

LikeLike

Your monetary education aligns with the Taylor rule! I think the FOMC did the right thing given the tenor of the times. Thenext meeting will not be as harmonious unless inflation recedes. Rubio should resign. It was a slap in the face that he was not one of the negotiators. As a senator he opposed Obama’s deal for giving concessions to a regime that always violates agreements and poses a threat to the US and its Gulf allies.

LikeLike

Your monetary education aligns with the Taylor rule! I think the FOMC did the right thing given the tenor of the times. Thenext meeting will not be as harmonious unless inflation recedes. Rubio should resign. It was a slap in the face that he was not one of the negotiators. As a senator he opposed Obama’s deal for giving concessions to a regime that always violates agreements and poses a threat to the US and its Gulf allies.

LikeLike

All I can add is fm Investopedia 2026:

…”Former Federal Reserve Chairman Ben Bernanke used similar arguments in responding to Taylor’s criticisms of the Fed’s monetary policy before and after the 2007-2009 global financial crisis. Given the limitations of the Taylor Rule formula, “I don’t think we’ll be replacing the FOMC with robots anytime soon,” Bernanke concluded….”

How about AI?..

Right now, I guess Warsh is waiting to see what happens to the economy with an end ( ? ) to the Iran conflict. I would think that situation is a stressed economy.

LikeLike

Taylor never said to use a monetary formula under all circumstances and Bernanke knew that and was trying to justify his interventionist policies. The question was whether the use of a monetary rule would have prevented the 2007-9 crisis from being as deep as it was had it been consistently applied in the years previous. Also Taylor would admit that under certain circumstances like COVID the rule would not apply.

LikeLiked by 1 person