When Is Transitory Transitory?

Remember when Janet Yellen and Jerome Powell declared that inflation was “transitory”? They were ultimately proven wrong. Their critics went ballistic, accusing them of lying to protect the Biden administration. Powell was branded a political hack—just as many had long viewed Yellen in her role as Treasury Secretary. But here’s the thing: they weren’t actually wrong at the time. They were relying on a specific measure of inflation that did, in fact, suggest the price surge was temporary. That measure—the Fed’s preferred gauge—was the Personal Consumption Expenditures (PCE) price index, not the better-known Consumer Price Index (CPI).

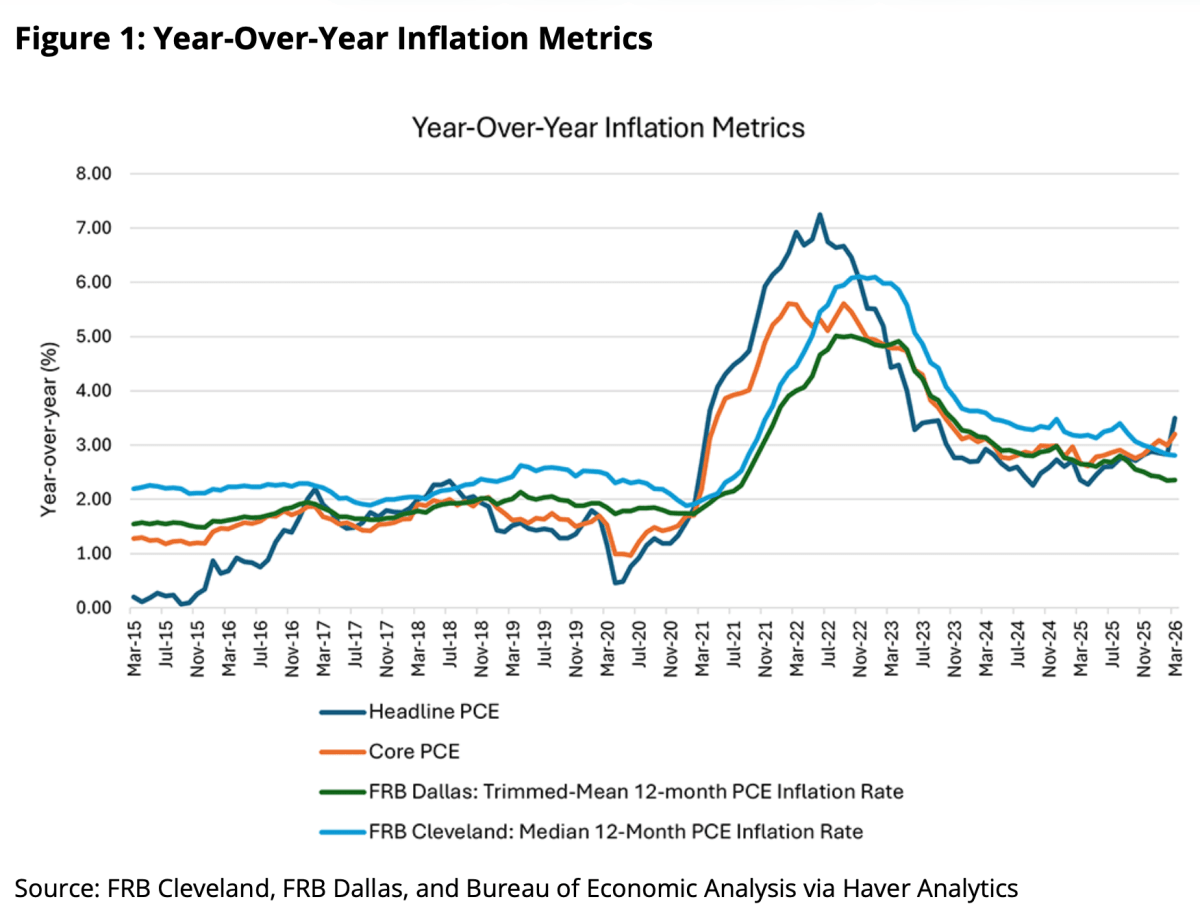

The PCE is similar to the CPI but differs in a few important ways. First, the PCE captures certain indirect purchases excluded from the CPI, such as medical care paid for by insurance. It also covers rural and urban consumers, nonprofits, and items purchased on behalf of consumers—like employer-provided fringe benefits. Second, and more critically, the PCE’s formula accounts for the fact that consumers adapt to rising prices by substituting lower-cost goods or services for more expensive ones. The PCE captures this substitution effect on an ongoing basis, while the CPI only updates its basket of goods and services every two years. The PCE is therefore more comprehensive than the CPI. But it excludes food and energy prices, which tend to be volatile due to temporary factors such as weather or geopolitical disruptions (think the Strait of Hormuz). Under this framework, if prices rose because of COVID-19—and were expected to fall once the pandemic subsided—policymakers would reasonably classify that inflation as “transitory.” And so they did.

There are other inflation measures worth knowing. The Producer Price Index (PPI) and the GDP deflator are two examples. The Dallas Fed computes something called a “trimmed mean PCE,” which strips out the top 31 percent of the fastest-growing price categories and the bottom 24 percent of the slowest-growing ones. There is also the Median PCE, which can be thought of as a more aggressive version of the trimmed mean—it symmetrically removes the top and bottom 50 percent of categories (sorted by spending-weighted growth rates), leaving only the category sitting precisely in the middle. Each measure has its proponents and detractors. Research suggests, for instance, that the Dallas Fed trimmed-mean measure was downwardly biased when price changes became more positively skewed during the inflation surge of 2021.

Why does any of this matter? Because monetary policy operates with a significant lag. My advisor Karl Brunner drilled this point into us, drawing on Milton Friedman’s landmark study A Monetary History of the United States and subsequent research. Friedman wrote: “There is much evidence that monetary changes have their effect only after a considerable lag and over a long period and that the lag is rather variable.” At the November 2022 Federal Open Market Committee (FOMC) meeting, Fed Chair Jerome Powell invoked this same concept of “long and variable lags.” The implication is straightforward: when the Fed acts—say, by adjusting the federal funds rate through open market operations—it takes considerable time before those actions ripple through to the broader economy. Friedman found that, averaged across the 18 business cycles studied, “peaks in the rate of change in the stock of money tend to precede peaks in general business by about 16 months and troughs in the rate of change in the stock of money to precede troughs in general business by about 12 months.”

That was then—what about now? Asset prices, such as stock prices and government bond yields, typically respond to changes in monetary policy within hours or even minutes. But those rapid asset-market reactions are far ahead of what happens to real goods and services prices and actual economic activity. Federal Reserve Governor Christopher Waller has noted that, in more recent cycles, lags tend to run nine to twelve months—shorter than in Friedman’s era, but still meaningful. Meanwhile, the president of the Kansas City Fed has warned that it may be a mistake to view the current rise in oil prices as “transitory,” even though Powell has suggested it might be. On the other side of that debate, Fed Governor Michelle Bowman has argued that reacting to temporarily elevated energy-price inflation would impose unnecessary restraint on the economy and labor market: “I am optimistic that, once the conflict is resolved, supply disruptions will ease, leaving a temporary imprint in [PCE] inflation and minimal impacts on domestic economic activity.” And yet the Cleveland Fed’s Beth Hammack, who sits on the Open Market Committee, has cautioned that waiting for definitive proof that inflation has become entrenched could force the Fed into larger, more disruptive rate adjustments down the road. Translation: if inflation stays above the 2 percent target, rate hikes will follow.

So it is noteworthy that in the Fed’s Open Market Committee there is significant disagreement over whether spikes in prices are transitory or not. Also should the Fed take action now because of those spikes that will have impacts not felt in real economic activity for a considerable while. Consider, it the spike is transitory and the Fed takes immediate action to raise rates, then the impact in the future will be less economic growth than otherwise.

To recap: different inflation measures produce different results. The Fed favors measures that filter out temporary price volatility because reacting to short-lived fluctuations—given the long lags involved—tends to produce suboptimal outcomes. I used to describe monetary policy to my students as turning around an aircraft carrier. Well, the U.S. economy is a $30 trillion aircraft carrier. If the price increases are concentrated in volatile categories likely to reverse on their own, the Fed will generally view them as transitory. That reasoning is sound—until it isn’t.

Enter Kevin Warsh, the new Fed chair, who wants to revisit the PCE as the primary inflation benchmark. Consider the divergence: the PCE’s “core” measure (excluding food and energy) ran at 3.3 percent over the past year, while the Dallas Fed’s trimmed mean came in at just 2.3 percent. If the Fed were to formally adopt the trimmed mean as its standard, it could declare victory and cut the federal funds rate—something that would surely delight President Trump. At his confirmation hearing, Warsh said: “What I’m most interested in is what’s the underlying inflation rate, not what’s the one-time change in prices because of a change in geopolitics or a change in beef.” That framing should also encompass Trump’s tariffs and the wave of geopolitical disruptions currently buffeting the global economy. If these shocks are truly one-offs, the trimmed mean gives the Fed less reason to tighten. If they are masking deeper demand pressures, these alternative gauges offer false comfort—and would expose the Fed to withering criticism if inflation resurges.

My concern is this: although Warsh has said all the right things about Fed models, the Fed’s historical overreach into fiscal policy, and the dangers of discretionary excess, his push to change the inflation benchmark looks uncomfortably like a search for whatever measure produces the lowest number. To be fair, Fed policy decisions are genuinely difficult—especially when long and variable lags mean that today’s correct call can easily become tomorrow’s mistake.

Here is a research paper that might be of interest.

The Long and Variable Lags of Monetary Policy: Evidence from Disaggregated Price Indices

By S. Borağan Aruoba and Thomas Drechsel

I now remember why I liked my hardest classes at 8am. Less brain fog…

What I glean from what you’ve catalogued is that the Fed is easily manipulated by all those who stand to gain transitory benefits (lower interest rates and a stock market kick), while someone lose takes the hit for the lag effect of the actions.

Proof once more of why we need adults in the room.

LikeLike

The point is that it is easy to be wrong – see the labor statistics. Even the best statistical model is often wrong and no one notices when you are right.

LikeLiked by 1 person

I now remember why I liked my hardest classes at 8am. Less brain fog…

What I glean from what you’ve catalogued is that the Fed is easily manipulated by all those who stand to gain transitory benefits (lower interest rates and a stock market kick), while someone lose takes the hit for the lag effect of the actions.

Proof once more of why we need adults in the room.

LikeLike

When Churchill said this, he was referring to the stock market: ….”the inherent probity and strength of the American speculative machine…. It is not built to prevent crises, but to survive them.” Economist 2025. Same article says markets are affected by WHO has access to Washington…

Macro shocks: Everything in motion remains in motion. unless affected by an outside force..

No matter what is affecting the cost of fertilizer. we must eat. And right now that depends on many transport systems, and the Middle East & Hegseth…

As mentioned Covid is a good indicator- based on an aggregate of responses…

While some stayed home eating fm boredom, some bought canned food , and washed every can. That meant expansive cooking menus with stretching ingredients—less purchases because washing cans is also boring..

Is beer a food? Modelo beer followed those crossing the border, illegal or not. Then , allegedly, illegal crossings stopped.

Illegals went home. But now Good Ole Americans started drinking Modelo.

In Modelo Land. the drop in purchase corrected, as Modelo became an American beer…

Transitory market ….maybe not , if an indicator that citizens were not returning to Guinness..

I’m glad blog essayist sometimes talks about beer.

LikeLike

Lies, damn lies, and statistics!

LikeLike

How about “Lied,damn lies, and damn statistics “?

LikeLike